Contribution Margin: What Is It and How To Calculate It

The resulting ratio compares the contribution margin per unit to the selling price of each unit to understand the specific costs of a particular product. The overarching objective of calculating the contribution margin is to figure out how to improve operating efficiency by lowering each product’s variable costs, which collectively contributes to higher profitability. To calculate the contribution margin, we must deduct the variable cost per unit from the price per unit. The Contribution Margin is the incremental profit earned on each unit of product sold, calculated by subtracting direct variable costs from revenue. Regardless of how contribution margin is expressed, it provides critical information for managers.

What is your current financial priority?

Soundarya Jayaraman is a Content Marketing Specialist at G2, focusing on cybersecurity. Formerly a reporter, Soundarya now covers the evolving cybersecurity landscape, how it affects businesses and individuals, and how technology can help. You can find her extensive writings on cloud security and zero-day attacks. Learn about the time interest earned ratio and how to calculate it. The following are the disadvantages of the contribution margin analysis.

Fixed cost vs. variable cost

At a contribution margin ratio of \(80\%\), approximately \(\$0.80\) of each sales dollar generated by the sale of a Blue Jay Model is available to cover fixed expenses and contribute to profit. The contribution margin ratio for the birdbath implies that, for every \(\$1\) generated by the sale of a Blue Jay Model, they have \(\$0.80\) that contributes to fixed costs and profit. Thus, \(20\%\) of each sales dollar represents the variable cost of the item and \(80\%\) of the sales dollar is margin. Using the above information the contribution margin per unit is $14 (the selling price of $20 minus the variable manufacturing costs of $4 and variable SG&A expenses of $2). Therefore, the contribution margin ratio is 70% (the contribution margin per unit of $14 divided by the selling price of $20). This contribution margin ratio tells us that 70% of the sales revenues (or 70% of the selling price) is available to cover the company’s $31,000 of monthly fixed costs and fixed expenses ($18,000 + $12,000 + $1,000).

Step 3 of 3

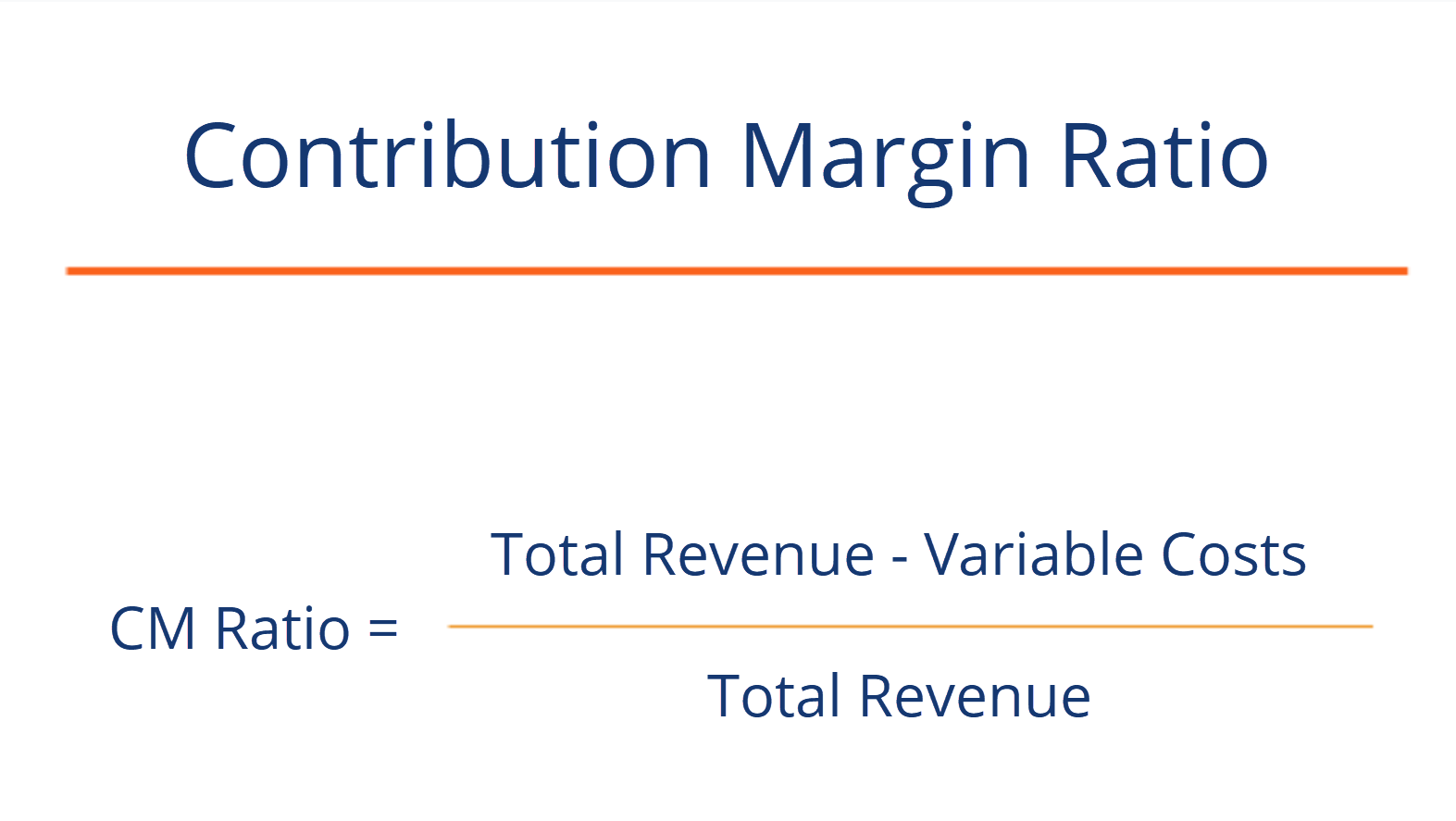

The contribution margin ratio is calculated as (Revenue – Variable Costs) / Revenue. Very low or negative contribution margin values indicate economically nonviable products whose manufacturing and sales eat up a large portion of the revenues. Investors examine contribution margins to determine if a company is using its revenue effectively. A high contribution margin indicates that a company tends to bring in more money than it spends. The contribution margin can help company management select from among several possible products that compete to use the same set of manufacturing resources. Say that a company has a pen-manufacturing machine that is capable of producing both ink pens and ball-point pens, and management must make a choice to produce only one of them.

Ask Any Financial Question

If the total contribution margin earned in a period exceeds the fixed costs for that period, the business will make a profit. If the total contribution margin is less than the fixed costs, the business will show a loss. In this way, contribution margin becomes an important factor when calculating your break-even point, which is the point at which sales revenue and costs are exactly even ($0 profit). This, in turn, can help you make better informed pricing decisions, but break-even analysis won’t show how much you need to cover costs and make a profit. A contribution margin ratio of 40% means that 40% of the revenue earned by Company X is available for the recovery of fixed costs and to contribute to profit.

Calculate Contribution Margin Ratio

If they send one to eight participants, the fixed cost for the van would be \(\$200\). If they send nine to sixteen students, the fixed cost would be \(\$400\) because they will need two vans. We would consider the relevant range to be between one and eight passengers, and the fixed cost in this range would be \(\$200\). If they exceed the initial relevant range, the fixed costs would increase to \(\$400\) for nine to sixteen passengers.

- The analysis of the contribution margin facilitates a more in-depth, granular understanding of a company’s unit economics (and cost structure).

- The break even point (BEP) is the number of units at which total revenue (selling price per unit) equals total cost (fixed costs + variable cost).

- One of the important pieces of this break-even analysis is the contribution margin, also called dollar contribution per unit.

If you want to reduce your variable expenses — and thereby increase your contribution margin ratio — start by controlling labor costs. The contribution margin is important because it gives you simple bookkeeping spreadsheet a clear, quick picture of how much “bang for your buck” you’re getting on each sale. It offers insight into how your company’s products and sales fit into the bigger picture of your business.

The electricity expenses of using ovens for baking a packet of bread turns out to be $1. The contribution margin is given as a currency, while the ratio is presented as a percentage. Variable costs tend to represent expenses such as materials, shipping, and marketing, Companies can reduce these costs by identifying alternatives, such as using cheaper materials or alternative shipping providers.

For example, analysts can calculate the margin per unit sold and use forecast estimates for the upcoming year to calculate the forecasted profit of the company. Labor costs make up a large percentage of your business’s variable expenses, so it’s the ideal place to start making changes. And the quickest way to make the needed changes is to use a scheduling and labor management tool like Sling. Variable expenses are costs that change in conjunction with some other aspect of your business. Cost of materials purchased is a variable expense because it increases as sales increase or decreases as sales decrease.